Learnings from cleantech 1.0 ⏳

Impact Supporters Issue #23. Thanks for being here. If you have comments or feedback drop me a message.

Disclaimer from August Solliv: Everything that I write here is my own opinion and my own research, and is not affiliated with any current or former employments i.e. it’s my weekend work 😉

Greetings, Impact Supporters! 🌍 It’s August Solliv 👋 This week we are diving deep into a part of the Impact VC history - namely cleantech 1.0! This is, in my opinion, the #1 history lesson to know for any climatetech investor today - so hope you’ll read along.

Cleantech 1.0 is often discussed when questioning whether climatetech investments today will truly be able to make satisfying returns. I was not in Impact VC when the cleantech 1.0 wave was ongoing, but I am a strong believer in “learning from your mistakes“, so I have analyzed the cleantech 1.0 wave to understand what learning can be taken from it for the current climatetech 2.0 wave 🔍 That analysis and research is what I am sharing with you today!

Note: This article is based on research from many different papers / articles. I have listed them all at the end of the article and cited them at specific points in the article when I quote or use specific numbers.

Agenda:

History of cleantech 1.0 📜

The emergence of climatetech 2.0 🚀

Returns in cleantech 1.0 💰

Why did it fail? 📉

Key learnings to remember today (what has changed and what hasn’t?) 🧠

Can climatetech 2.0 create successful returns? ✅

History of cleantech 1.0 📜

The cleantech 1.0 wave took place from 2006 to 2011, primarily in Silicon Valley, and consisted of a series of investments in energy start-ups. It was a reaction to rising oil and gas prices, increasing amounts of government subsidies for climate solutions, as well as a realization of the need to act on climate change led by Al Gore’s strong public statements on the topic 🌞💨 Between 2006 and 2011, it’s estimated that VC investors poured approximately $25 billion into cleantech, peaking at just below $6 billion invested in 2008 (MIT, 2016).

The wave was primarily led by generalist tech investors and a couple of biotech investors who focused on energy generation. They invested in manufacturing and new technologies in sectors like solar, wind, biofuels, and fuel cells that required significant upfront investment and were highly unproven at the time (MIT, 2023)🌱

Source: MIT, 2016

The cleantech 1.0 wave failed to deliver the returns that VC investors expected and new investments pretty much died after 2011. Some of the largest failures were solar manufacturing startups like Solyndra, compressed air energy storage ventures like Lightsail, concentrated solar power outfits like Brightsource, and battery-swapping networks like Better Place. There were still some winners like Tesla, Sunrun, and Enphase, but these couldn’t outweigh the large number of failures (Next Ascent, 2022) 📉

The emergence of climatetech 2.0 🚀

Let’s finish up the history deep-dive before going into the details of what failed/ succeeded during cleantech 1.0.

After cleantech 1.0, it was consensus that investing in cleantech was doomed to fail. A canonical article from MIT made it clear that cleantech start-ups weren’t able to make VC returns (MIT, 2016). It took until 2020 for the enthusiasm around cleantech to pick up again, but it came back strongly 🌟 This time not under the name cleantech but rather climatetech (so cleantech 2.0 doesn’t exist). Climatetech 2.0 is currently underway. In 2021, investors invested $37 billion in climatetech and according to CTVC, there was $300 billion of dry powder raised in 2022 (not all VC money). According to BCG, $100 trillion-$150 trillion of additional investments across asset classes will be necessary by 2050 to accelerate the world to net-zero (B Capital, 2023) 🌍💼

As can be seen on the graph below, climatetech has seen strong growth, but the growth has decreased in recent years together with the crisis in the industry at large. However, compared to other sectors, climatetech is still doing well and has the potential for increasing investments when the economic conditions change.

Source: CTVC, 2024

Returns in cleantech 1.0 💰

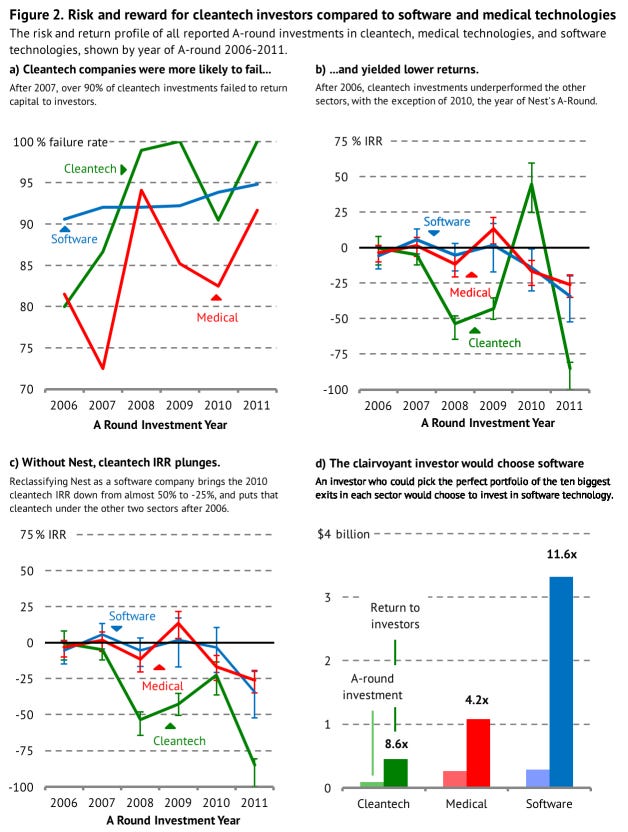

Simply put, cleantech 1.0 was a VC failure. It is estimated that nearly half of the $25 billion capital invested by funds between 2006 and 2011 was either lost or impaired. More than 90 percent of cleantech companies funded after 2007 ultimately failed to return just the initial capital invested. And when comparing with the general tech sector as well as the medtech sector, cleantech 1.0 pretty much underperformed on all parameters (see image below). The biggest money losers for VCs were start-ups developing new materials, hardware, chemicals, or processes (MIT, 2016) 💔

So why did cleantech 1.0 fail so heavily? Read on for the key insights.

Why did it fail? 📉

Many things have been said about why cleantech 1.0 start-ups failed and VCs pulled out from the sector. I have tried to summarize the main points that I have read (non-exhaustive list):

🏛️ The external environment changed with 1. the financial crisis removing subsidies, 2. oil prices declining making it harder for renewables to be cost competitive, and 3. the price of energy declining strongly with China flooding the solar market with cheap solar panels and the development of the fracking technology

💸 VCs invested in capital-intensive hardware with poor economics that didn’t reach scale often in low-margin industries

🔭 Some VCs were relatively new to working with technology risk and misjudged long development and scaling timelines (above the 3-5 year classical VC time horizon)

🚪 VCs couldn’t exit their investments as corporates didn’t buy up the risky startups and follow-on capital dried up

Key learnings to remember today (what has changed and what hasn’t?) 🧠

The challenges of commercializing climatetech 2.0 start-ups compared to cleantech 1.0 start-ups are pretty similar. Many start-ups still have a lot of hardware components and high technology risks. The economics might be slightly better as solutions are often a mix of hardware and software compared to pure hardware solutions during cleantech 1.0, but some VCs argue that they are very similar (MIT, 2023) ⚖️

So it is key to retain some key learnings from cleantech 1.0 to avoid making the same mistakes in climatetech 2.0 💼 The one major learning is very simple. David Rotman puts it as (MIT, 2023):

Lesson #1: “The survival of climatetech startups depends on demand for their inventions from large and expanding markets.”

David Rotman highlights 5 further lessons in his article for MIT Technology Review in December 2023:

Lesson #2: Hubris hurts - Do not have people invest in a category who do not know about the category.

Lesson #3: Molecules are different from bits - Finding out whether a hardware process is commercially competitive typically means building a demonstration plant, often costing $100 million or more.

Lesson #4: The real takeaway from Solyndra - All start-ups need to be able to prove that they can be manufactured at large scale. Solyndra lacked market savvy and manufacturing flexibility and thus failed.

Lesson #5: Politics can change everything - Back in 2010, Massachusetts voters elected a Republican senator after the death of a Liberal one. This doomed a comprehensive climate bill and changed outlooks for cleantech 1.0 start-ups. Today, e.g. a Republican president would change climate subsidies significantly, and in Europe, some subsidies are disappearing (link).

Lesson #6: Survival is all about the economics - “The brilliance of many new climate technologies is evident, and we desperately need them. But none of that will ensure success. Venture-backed startups will need to survive on the basis of economics and financial advantages, not good intentions.”

Can climatetech 2.0 create successful returns? ✅

The major question you might be asking yourself is: If climatetech 2.0 is so similar to cleantech 1.0, why should climatetech 2.0 start-ups be able to create successful returns when cleantech 1.0 start-ups couldn’t? 🤔 I have compiled a list of some reasons for why they could, below - but of course only time will tell:

Consumer attitudes and behavior are shifting toward sustainability 🌱

Corporate and government pledges toward net zero have reached critical mass and require climatetech start-ups to be reached 🌐

Cleantech 1.0 was centered on pioneering innovations within the energy sector (e.g. solar energy and biofuels). In contrast, climatetech 2.0 spans various industries, e.g. transportation, agriculture, industry, construction, etc. 🧠

Climatetech 2.0 has already proved that start-ups can reach successful exits 🚪

Climatetech 2.0 investors are mixing deep scientific knowledge with a VC investor skillset to be able to better assess climatetech start-ups 🔭

Other types of investors have a growing appetite to fund expensive and risky scale-up projects (buyout funds, corporations, growth funds, etc.) 💸

There are of course still challenges 🧩 The major one is that greenhouse gas externalities are still not appropriately priced globally in all industries. This limits market growth for climatetech start-ups and can prove to be a barrier to climatetech 2.0 start-ups’ financial returns (MIT The Engine, 2020).

Let’s see what will happen in the next years… I hope you liked the article and will keep these history lessons in mind when reflecting on the current climatetech 2.0 wave.

Please subscribe to stay updated on articles about everything related to impact VC - and share with friends and colleagues. See you next week for another issue! 👋

Sources:

Brilliant!