A recipe for building an impact VC fund thesis 📋

Impact Supporters Issue #37. Thanks for being here. If you have comments or feedback drop me a message.

Disclaimer from August Solliv: The views expressed are solely my own, i.e., it’s my Sunday fun work 😉

Greetings to 2k+ Impact Supporters! 🌍 It's August Solliv 👋 This week I have tried to create a summary of all the choices you have to make as a GP when building an impact VC fund thesis - whether you are a traditional GP transitioning into impact or a dedicated impact VC GP - whether this is your first fund or impact fund number 4 - whether you are a climate or social impact fund, etc. (reading time ≈7min)

This is not a perfect and final list but is the current version and will hopefully be work in progress over some months/years (I actually wrote a similar piece last year but with a broader focus - see the end of the article to find it) - and I want to hear from you what other complementary choices you think are key - feel free to add them in the comments or my DMs 📩

I have structured the article/recipe in three parts: 2 key questions to answer, 10 core choices to make, and finding an edge.

What sets you or your fund apart? 🫵

There is one question that GPs will always have to answer to attract capital from LPs and show relevance to impact start-ups:

Why is/are the GP(s) the right one(s) to build this fund and invest in impact start-ups?

This should be a one-liner and sit at the tip of the tongue of any VC (impact or traditional). In general, it comes down to two things: Either you understand a sector or segment better than anyone so you make the best investment decisions, or you have a unique network that gives you access to an abnormal amount of deals. These elements can give you a true advantage when investing and can be identified through your track record 📊

Moreover, in impact VC a second key question is:

What is the market gap that the fund is filling?

The market gap that the impact fund is filling is key as the impact VC industry is still a fairly nascent industry, which has some key large market gaps. However, you could argue that you don’t necessarily need to fill a market gap to build an impact VC fund if you believe that you can invest better than the competition (i.e. answer question 1 well). It will still help you fundraise if you are filling a market gap 🌱 Two examples of major impact VC market gaps are:

Capital for impact growth businesses. In recent years early-stage impact start-ups have received major parts of VC capital and today these are arriving at growth stage but there are few impact growth investors ready to take them from Series B+ to IPO/trade sale/buyout. The market gap has been mentioned in many of my previous interviews - to mention a couple check out the ones with Remi Saïd (Partech Impact) and Dougie Sloan (Better Society Capital)

Capital for underfunded climate sectors. Since the appearance of climatetech investments in the last 5-10 years, some sectors have been “overfunded“ compared to their share of total GHG emissions in the world. There is a market gap for impact VC investments in “Agriculture“, “Industry“ and the “Built Environment”. Check out the article with Christian Jølck from 2150 about how they invest in the market gap in the Build Environment.

Source: PwC State of Climatetech report, 2022

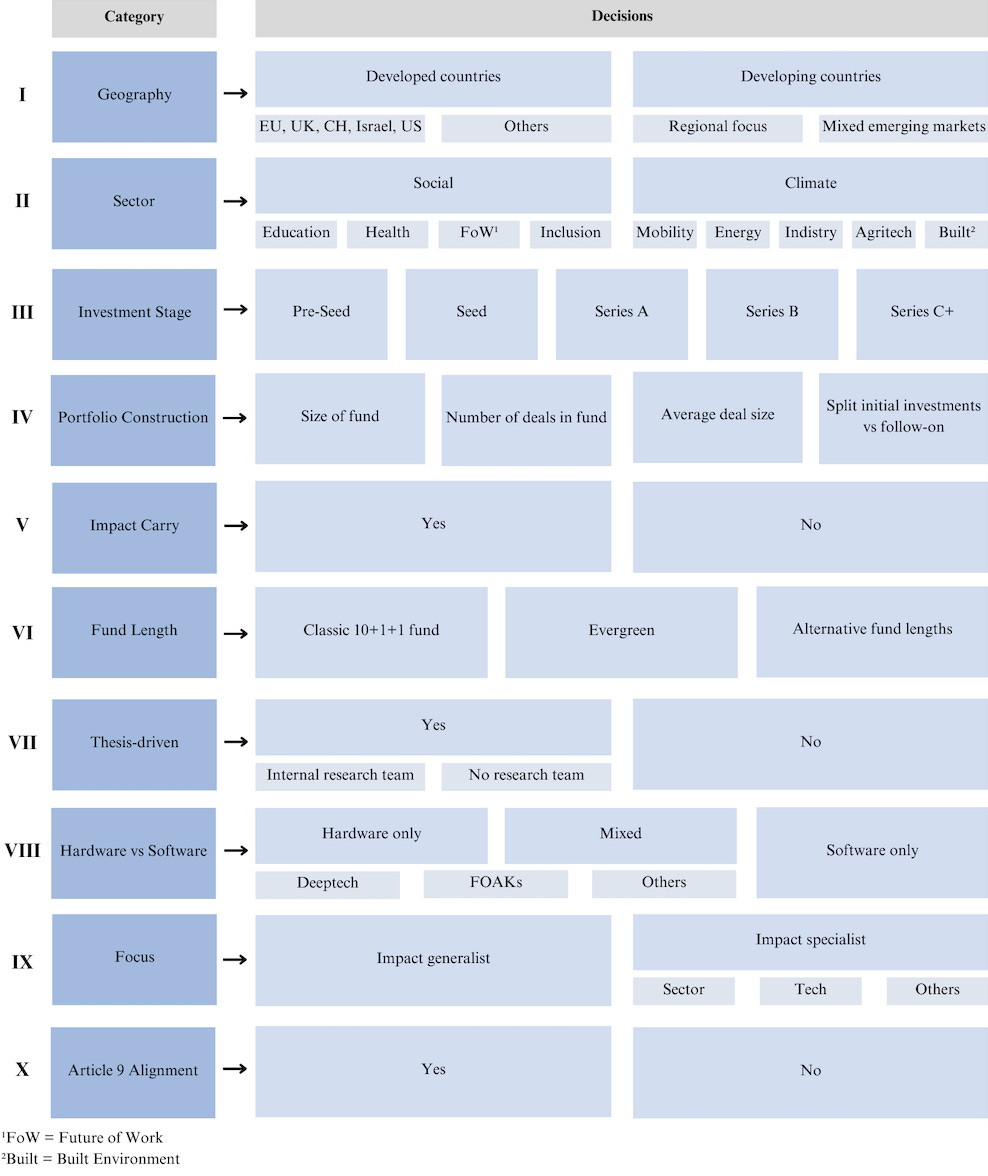

🔟 Core choices

I have mapped the core investment thesis choices that impact VCs have to make. This is the core of the recipe 📋 See the 10 categories in the graph below:

Here are my key points to the categories:

🌍 Geography - The typical geographical focus for European impact VC funds has been the EU + one or two countries among the UK, CH, the US, and Israel. When thinking about geography, it is key to consider what sovereign funds you hope to raise funds from - they usually have requirements for a % of the total value of deals that needs to be made in a specific country. Likewise, the EIF often has requirements for what % of the fund is deployed in the EU. Some impact funds also invest in developing markets as they see the impact being higher there.

🗂️ Sector - To build an impact investment thesis, VCs have to define their focus sectors. It can be everything across both the social and climate areas or specific sectors but the more the less sector-specific knowledge the fund can have.

🧮 Investment Stage - All impact VCs must define at what stage they invest in impact start-ups. This also defines the DD process for start-ups afterward.

🏗️ Portfolio Construction - A key part of the thesis relies on portfolio construction and what returns the impact VC aims for. The portfolio construction decisions are dependent on other factors such as geography and investment stage so must be made in relation with those.

💸 Impact Carry - Impact carry is a double-filtered carry where GPs must meet impact KPIs as well as financial KPIs to get carry paid out. The EIF has built the most used model for impact carry that they ask most of their funds to use to receive an investment from them. Impact VCs must decide whether they want to link their carry to their impact.

⏳ Fund Length - When building their investment thesis, impact VCs must decide whether they believe that impact start-ups need more patient capital to develop and if yes, whether they believe different fund lengths can help unlock extra value in the impact VC model.

🕵️ Thesis-driven - Some major impact VCs are thesis-driven, often having internal research teams, to make sure they make the right bets in key sectors. This is especially prevalent in climate VC as they are very science and deeptech heavy.

👩🏭 Hardware vs Software - Impact VCs must decide whether they believe that they can make exceptional returns on both hardware and software and whether to include both in their investment scope. More and more climate VCs include hardware as they say that it is very hard to fix a physical problem (i.e. climate change) without physical solutions.

👆 Focus - As the impact VC market is maturing, impact VC funds must ask themselves if it has more value to specialize in one or more sectors to build strong enough expertise in the areas they invest in.

💚 Article 9 alignment - Impact VCs must decide whether they want to become an Article 9 fund as it adds reporting and structure requirements to the fund but also unlocks a large chunk of LP capital.

Finding an edge 🌟

Apart from the core thesis choices that impact VC investors make, many impact VC funds try to find their own edge 🌟 (sometimes linked to the question “Why is/are the GP(s) the right one(s) to build this fund and invest in impact start-ups?“ and sometimes not). This is also part of the total recipe 📋 I have listed examples below for your inspiration:

Building an internal science team (Planet A)

Building an impact VC fund on top of an impact community (Voyager VC, MCJ Collective, and Norrsken VC)

Investing in commons as part of your VC investments to revolutionize the VC model (2050)

Building a partnership with a recognized voice in a sector (Racine^2, Serena VC’s partnership with Makesense and Heka, Newfund’s partnership with FoundaMental Foundation)

Working with a double impact layer - investing in diverse founders on impact topics (Unconventional Ventures)

Defining specific categories of companies that you invest in, e.g. hard tech (Climentum Capital), or only focusing on gigacorns (Extantia)

Using VC as just one tool out of many in a systems change impact toolbox that give many options to impact entrepreneurs (Maze)

So, that was the high-level impact VC fund thesis recipe 📋 I would love to hear from you - what do think about the recipe? What more would you add? I am sure there are more categories to add :)

Without making the article very long it’s hard to be fully extensive - here are a couple of other categories that I thought about: debt vs equity, the impact of the LP base on the investment thesis, other areas to be unique in (e.g. specific DD processes, or specializing in relationships with unis).

Thanks for reading this week’s newsletter! Let me know what you think of this article - either in the comments section or in my DMs. Please subscribe to stay updated on articles about everything related to impact VC - and share with friends and colleagues. See you next week for another issue! 👋

This was actually the second time I published a view on the decisions that impact VCs can and must make. This one was more narrowed down and covers the space in my opinion. You can see the original here:

🔍 Creating an impact VC methodology

You are reading Issue #1. Thanks for being here. If you have comments or feedback, drop me a message 🧑💻

Adding an extra VC fund based on comments from LinkedIn:

"4P Capital believes marketing and sales are key drivers in early stage investing, especially when scaling impact. We invest in environmental and social resilience"

Adding an extra VC fund based on a comment from Sara Sande on LinkedIn:

"I would add EIFO to the list for being able to come with mixed financing - impact startups would often need a mix of equity, venture debt, debt and/or project financing from patient investors. We are able to support companies all the way with the right funding mix."